What is Sequence of Returns Risk?

Arguably one of the least discussed, but critically important risks to long-term retirement success, Sequence of Returns Risk is an important consideration for many individuals and families as they approach and enter retirement. For those currently in or approaching retirement, it’s a risk that’s important to consider.

The #1 Hidden Retirement Risk You May Not Be Aware Of

By: Scott Sturgeon, JD, MBA, CFP®

Would you like to receive more content just like this directly to your inbox? Click here to subscribe!

After working, saving and investing for decades, you’re finally reaching a point where retirement is on the horizon. Maybe that means leaving a full-time job to do some consulting work on the side. Maybe it’s finally pursuing that hobby you’ve been passionate about for years, but just haven’t had the time to do. It could even be something as simple as finally learning to cook or spending more time with your children or grandchildren. With all these exciting possibilities, Sequence of Returns Risk is probably not on the top of your radar of things to lookout for in retirement, but it should be.

Whatever retirement looks like for you, there’s a strong likelihood that many of those decisions are going to be based on your ability to generate cashflow from your investment accounts to fund your lifestyle in retirement. Cash savings, social security, pensions, taxable brokerage accounts, Individual Retirement Accounts (IRA’s), Roth IRA’s, 401(k)’s and a variety of other workplace retirement plans may all be pieces you’re trying to incorporate together to meet your cashflow needs. While the tax implications of drawing on each of those account types is undoubtedly an important part of a comprehensive retirement plan, Sequence of Returns Risk is arguably just as important of an item to consider.

Sequence of Returns Risk is basically the idea that the order of returns you experience across your various investment accounts in retirement is important. Your order of returns can have a major impact on your ability to generate adequate cashflow and sustain those assets over time. If you retire and immediately experience 5 years of poor or negative returns in your portfolios, it may have a significant impact on your long-term financial plans. If the same individual instead experiences those same negative or poor returns later in life, their overall financial plans are far less likely to be affected.

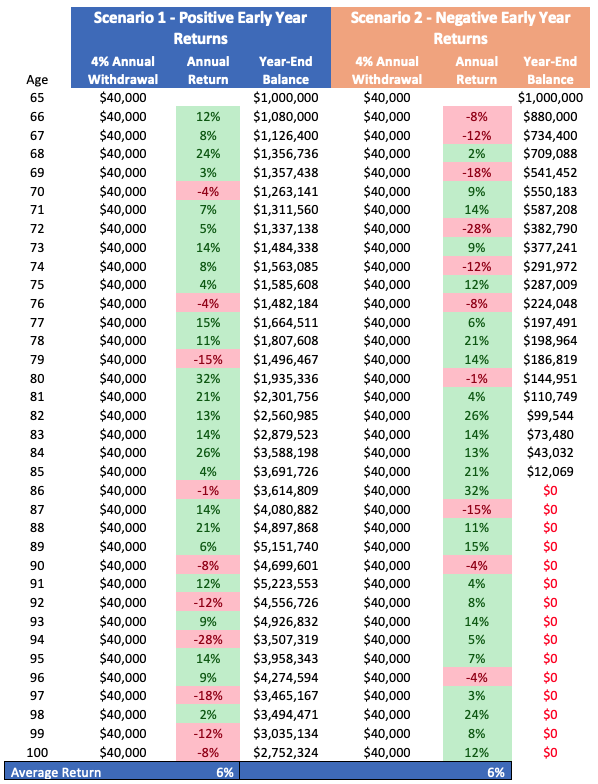

The accompanying diagram helps to illustrate this concept. If you hypothetically have $1 million spread across your various retirement accounts, retire at age 65, and your portfolios generates on average a 6% return through age 100, order of returns matters. Note that the order of returns for these two scenarios are actually the same, but in reverse order.

In Scenario 1, many of the initial years of retirement are highlighted by positive market returns. In Scenario 2, several of the lower or negative return years occur earlier in retirement, creating a profound impact on the long-term sustainability of making $40,000 annual withdrawals from your portfolio. In Scenario 2, the portfolio is completely diminished after 20 years, which is likely not a good outcome for a retiree living off that portfolio.

Steps you can take to prepare for Sequence of Returns Risk

So what can be done to mitigate Sequence of Returns Risk? That answer is really going to depend on you and your family’s specific financial situation, but there are a few high-level principles to consider.

Have a Plan

First, ensuring you have a retirement withdrawal strategy in place is important for covering whatever your projected living costs will be long term. If you’re planning to spend $100,000 per year on average, but in year 1 of retirement want to spend an additional $15,000 on a new patio, plus another $3,000 on outdoor furniture and the latest model of electronic smoker, taking that one-time additional expense into account is important. Having the ability to project how these kinds of sustained withdrawals and one-off scenarios are going to impact the success or failure of your long-term financial plans is critical.

Reduce Your Risk

In retirement, you win by not losing. When you were younger, you were able to invest aggressively because any volatility in your portfolio didn’t really matter as you weren’t typically pulling any money out of your accounts. Time was on your side for your portfolio to overcome any short-term losses.

In retirement, there’s usually not as much of a need to take on greater amounts of risk in your investments as you may have in younger years. If in the past you’ve tried to time the market, buy ‘hot stocks’, or otherwise make large speculative investments, when you’re approaching retirement, it may be better to reduce the amount of risk in your investment portfolio. Ensuring that you have an asset allocation that best reflects your retirement goals and objectives is important to ensuring you’re taking the least amount of risk necessary to achieve the target returns you may need.

Tax Planning 101

When it comes time to begin withdrawals from your various investment accounts to fund your lifestyle in retirement, each one may have a different way that it impacts your overall tax situation. That’s important because the amount you pay in taxes on retirement withdrawals directly reduces your net returns and the amount of money you’re able to withdraw from those different accounts. For example, a $1,000,000 IRA doesn’t actually have $1,000,000 that you can withdraw because a significant chunk is going to be withheld for state and federal taxes when you make withdrawals.

Creating a tax planning strategy at the start of retirement can potentially help to reduce the total amount of taxes you pay in retirement. The ultimately strategy you should implement is going to be highly contingent on what your overall makeup of various income streams, pre-tax, taxable, and tax-free retirement accounts you have. Making sure all those account types are working together in unison is key to minimizing your tax burden over time.

Allocation is Key

One of the greatest determining factors of how your investment portfolio will perform over the long term is your asset allocation. An asset allocation is essentially the makeup of different asset classes and types of assets that comprise the full balance of your portfolio or a given account. For example, your IRA might be invested 50% in stocks and 50% in bonds, so your allocation for that account is 50:50 stocks to bonds.

Ensuring your asset allocation across all your investment accounts is properly established relative to your risk tolerance, risk capacity, tax situation, spending needs and long-term plans is important. Your asset allocation is going to be one of the biggest determining factors in what your investment returns will look like throughout your retirement. Perhaps just as importantly, you overall asset allocation will dictate the amount of risk you’re taking to achieve those projected returns. In retirement, taking on the least amount of risk possible to achieve the return needed to support your lifestyle is a generally a good approach to ensuring you can make sustainable withdrawals in retirement.

While it may sound intimidating at first, Sequence of Returns Risk is a threat that can generally be reduced through proper financial planning. The first step though, is ensuring you have a financial plan that’s custom to you and your family’s individual needs. Working with an advisor can be helpful in that process to ensure you’re making sound financial decisions and working with an advocate who has your best interests in mind.

Curious to learn how working with a seasoned CFP® professional at Oread Wealth Partners can bring value to your unique financial situation? Let’s talk.

Subscribe To Our Newsletter Here

The Benefits of Hiring a CERTIFIED FINANCIAL PLANNER™

Oread Wealth Partners, LLC (“Oread Wealth Partners”) is a registered investment adviser offering advisory services in the State of Kansas and in other jurisdictions where exempted. Registration does not imply a certain level of skill or training. The presence of this website on the Internet shall not be directly or indirectly interpreted as a solicitation of investment advisory services to persons of another jurisdiction unless otherwise permitted by statute. Follow-up or individualized responses to consumers in a particular state by Oread Wealth Partners in the rendering of personalized investment advice for compensation shall not be made without our first complying with jurisdiction requirements or pursuant an applicable state exemption.

All written content on this site is for information purposes only. Opinions expressed herein are solely those of Oread Wealth Partners, unless otherwise specifically cited. Material presented is believed to be from reliable sources and no representations are made by our firm as to another parties’ informational accuracy or completeness. All information or ideas provided should be discussed in detail with an advisor, accountant or legal counsel prior to implementation.

Past performance may not be indicative of future results. Investing in securities involves risks, including the potential for loss of principal. There is no guarantee that any investment plan or strategy will be successful or that investments and markets will perform as they have in the past.